A fragile ceasefire agreement in the war began with bombs continuing to explode in Lebanon and contradictory statements about whether Iran will continue to control the critical Strait of Hormuz energy chokepoint.

But the most likely scenarios moving forward involve either Iran exerting more control over global energy markets than it did before the fighting started in March, or the current tenuous agreement merely delaying another military escalation by days or weeks, geopolitical and energy experts said.

There is a less likely, “happy scenario” where global energy trade returns to normalcy—but even that will take until the end of this year because of supply chain challenges—and where Iran is left weakened and militarily degraded for the long term, said Bob McNally, former White House energy advisor under George W. Bush and founder of Rapidan Energy Group.

“We think the odds favor this ceasefire either not ever sticking or unraveling if it does,” McNally told Fortune, arguing the April 7 announcement of a two-week ceasefire was vague, fragile, and contradicted by Iran—not exactly justifying oil prices falling by almost $20 per barrel overnight.

“The only thing we know for sure is the president called off a larger attack,” McNally said. “I am amazed at the market’s willingness to price in relief so willingly. While we do see a ceasefire as an ultimate end state, we don’t think we’re there yet, and we think this is going to get worse before it gets better.”

Hours after President Donald Trump issued profanity-laden messages threatening that Iran’s “whole civilization will die” in one night on April 7, he announced a two-week ceasefire in exchange for opening the narrow Hormuz waterway through which about 20% of global energy supplies transit. Iran agreed to open the strait but only “via coordination with Iran’s Armed Forces and with due consideration of technical limitations.”

Iran said it could continue to charge tolls per vessel, while Oman, which is situated on the other side of the strait, said “no fees will be imposed”—yet another contradiction.

Regardless, Israel, which was unhappy about the ceasefire, continued to attack Lebanon on April 8, and Iran kept the strait closed and threatened to withdraw from the ceasefire.

If the ceasefire does hold, Vice President JD Vance, special envoy Steve Witkoff and Jared Kushner are scheduled to travel to Islamabad for in-person negotiations with Iran on April 11, White House press secretary Karoline Leavitt said.

What happens next

Rystad Energy chief economist Claudio Galimberti sees an enduring ceasefire as the most likely scenario, but it won’t be pretty. Iran is likely to assert its control over the strait for at least a few months before any broader, long-term deal is reached with the U.S. and neighboring, oil-producing Gulf states.

“The normalization of the Strait of Hormuz is still far, far away,” Galimberti fold Fortune. “It’s a very fragile situation.”

He agreed that regular flows through the strait are unlikely at least until late 2026. In the meantime, a stronger ceasefire could mean the resumption of about one-third of the vessel traffic through the strait.

Traffic for oil, liquefied natural gas, fertilizer for agriculture, hydrogen for semiconductors, and petrochemicals plunged to 5% of typical flows in March and only grew to nearly 10% for a few days in early April before ceasing again on April 8.

Only a single Iranian-linked oil tanker passed through the strait on April 8, said Rohit Rathod, senior analyst with the Vortexa cargo tracking firm.

A lot of work remains. First, the strait would have to be cleared of mines and emptied of the hundreds of ships that have remained trapped for over a month. Then, vessels would need to resume their complicated, global logistical dance. And, eventually, Saudi Arabia, Iraq, Kuwait, the United Arab Emirates, and other Gulf states would restart their oil and gas production volumes—all of which would take many months, Galimberti said.

Oil prices—down to about $94 a barrel from over $110 the day prior—could continue to fall but remain elevated from pre-March levels by at least $10 per barrel longer term, including from higher insurance costs on tanker journeys, he said.

“The political risk premium is going to be embedded for a long time,” Galimberti said.

A return to the normal transit system of goods and commodities means ensuring insurance availability, commercial trade financing, and the resumption of empty, inbound “ballasting” vessels.

While the currently trapped ships will want to exit as quickly as they can, resuming other traffic is much harder, said Alan Gelder, senior vice president for refining, chemicals, and oil markets with the Wood Mackenzie energy research firm.

“[Inbound] ballasting vessels are unlikely to enter via the Strait of Hormuz any sooner than a ‘just in time’ logistics basis, at risk of becoming trapped if hostilities resume,” Gelder added.

As for the liquefied natural gas (LNG) exports, which mostly come from Qatar, shipments could be back up and running by the end of the summer, but more than 15% of its export capacity will remain offline for years because of serious damages inflicted from Iranian attacks.

In the meantime, McNally sees investors and energy traders overreacting to the ceasefire—as evidenced by the big spike in stock markets and the opposite drop in oil prices.

“The market was eager to hear a ceasefire had been reached. And the market continues to underappreciate the gravity and the risk of a prolonged disruption from Hormuz,” McNally said. “I still think there’s an unwarranted, large reservoir of hope and optimism that you see reflected in prices today.”

The next time you’re out to dinner, someone might not only ask to take your jacket, they may want you to hand over your phone, too. The number of bars and restaurants establishing a phone-free environment is growing, per Axios—a change that appeals to younger patrons.

Axios found that at least 11 states have individual restaurants or bars with a form of phone restriction or digital detox. Scrolling a menu instead of your phone is thought to create a more intimate setting, lead to more focus on food, and protect patron privacy.

A recent survey from Talker Research shows a significant number of people are putting their phones away and probably don’t want to see someone taking pictures of their food:

63% of Gen Z says they intentionally disconnect; 57% of millennials say the same.

Even older crowds are on board—42% of Gen X and 29% of boomers said they unplug.

A needed break: Data from Consumer Affairs showed Americans spend an average of 4.5 hours per day on their devices. Another revealed that 86.5% of phone use involves social networking and texting during meals.

It’s chains, too: The upscale supper club Delilah’s has a no-phones policy. Even some Chick-Fil-A locations are offering free ice cream as an incentive for turning over your phone while eating.—DL

The Fortune 500 Innovation Forum will convene Fortune 500 executives, U.S. policy officials, top founders, and thought leaders to help define what’s next for the American economy, Nov. 16-17 in Detroit. Apply here.

Imagine you tell an AI agent to convert $10,000 in U.S. dollars to Canadian dollars by end of day. The agent executes — badly. It misreads parameters, makes an unauthorized leveraged bet, and your capital evaporates. Who’s responsible? Who pays you back?

Right now, nobody has to. And that, a group of researchers argues, is the defining vulnerability of the agentic AI era.

In a paper published on April 8, researchers from Microsoft Research, Columbia University, GoogleDeepMind, Virtuals Protocol and the AI startup t54 Labs have proposed a sweeping new financial protection framework called the Agentic Risk Standard (ARS), designed to do for AI agents what escrow, insurance, and clearinghouses do for traditional financial transactions. The standard is open-source and available on GitHub via t54 Labs.

We are talking about an entire “agentic economy” here, t54 founder Chandler Fang told Fortune in an emailed statement; “it is very different from simply using AI agents for financial tasks.” He said there are two fundamental types of agentic transactions: human-in-the-loop financial transactions and agent-autonomous transactions. Everyone’s focus is on the human-in-the-loop stuff, he said, and that’s a real problem, because the financial ecosystem currently has no way to operate other than to defer all liability back to a human. It all comes down to the probabilistic nature of this technology, the researchers explained.

The probabilistic problem

The core problem the team identifies is what they call a “guarantee gap,” which they define as a “disconnect between the probabilistic reliability that AI safety techniques provide and the enforceable guarantees users need before delegating high-stakes tasks.” This description recalls what leadership expert Jason Wild previously told Fortune about how AI tools are probabilistic, befuddling managers everywhere. “Without a way to bound potential losses,” the t54 team wrote, “users rationally limit AI delegation to low-risk tasks, constraining the broader adoption of agent-based services.”

Model-level safety improvements, they argue, can reduce the probability of an AI failure, but cannot eliminate it. Large language models are inherently stochastic, meaning that no matter how well trained or well tuned an AI agent is, it can still hallucinate and make mistakes. When that agent is sitting on top of your brokerage account or executing financial API calls, even a single failure can produce immediate, realized loss.

“Most trustworthy AI research aims to reduce the probability of failure,” said Wenyue Hua, Senior Researcher at Microsoft Research. “That work is essential, but probability is not a guarantee. ARS takes a complementary approach: instead of trying to make the model perfect, we formalize what happens financially when it isn’t. The result is a settlement protocol where user protection is deterministic, not probabilistic.”

The researcher’s solution borrows directly from centuries of financial engineering. ARS introduces a layered settlement framework: escrow vaults that hold service fees and release them only upon verified task delivery; collateral requirements that AI service providers must post before accessing user funds; and optional underwriting — a risk-bearing third party that prices the danger of an AI failure, charges a premium, and commits to reimbursing the user if things go wrong.

The framework distinguishes between two types of AI jobs. Standard service tasks — generating a slide deck, writing a report — carry limited financial exposure, so escrow-based settlement is sufficient. Tasks involving the exchange of funds — currency trading, leveraged positions, financial API calls — require the agent to access user capital before outcomes can be verified, which is where underwriting becomes essential. It is the same logic that governs derivatives markets, where clearinghouses stand between counterparties so that a single default doesn’t cascade.

The paper maps ARS explicitly against existing risk-allocation industries in a table: construction uses performance bonds, e-commerce uses platform escrow, financial markets use margin requirements and clearinghouses, and DeFi uses smart contract collateralization. AI agents, the researchers argue, are simply the next high-stakes service category that needs its own version of that infrastructure.

The timing is crucial

Financial regulators are already circling. FINRA’s 2026 regulatory oversight report, released in December, included a first-ever section on generative AI, warning broker-dealers to develop procedures specifically targeting hallucinations and to scrutinize AI agents that may act “beyond the user’s actual or intended scope and authority”. The SEC and other agencies are watching closely.

But ARS is pitched as something regulators haven’t yet built: not a set of rules, but a protocol — a standardized state machine that governs how funds are locked, how claims are filed, and how reimbursements are triggered when an AI agent fails. The researchers acknowledge ARS is one layer of a larger trust stack, and that the real bottleneck will be building accurate risk-pricing models for agentic behavior.

“This paper is the first step in setting up a high-level framework to capture the end-to-end process associated with agent-autonomous transactions and what the risk assessment looks like,” Fang told Fortune. “Further down the road, we should introduce more specific details, models, and other research to understand how we figure out risk across different use cases.”

Donald Trump Jr. lashed out at the European Union on Tuesday, saying its liberal policies were discouraging investment and predicted a “major fracture” between the bloc’s eastern and western member states.

The eldest child of the U.S. president said that “the biggest players, the biggest names in banking and finance, in tech and AI across the board” believe that “Europe is a disaster,” but “the disaster that they feel also needs to be fixed.”

“The only way it gets fixed, though, in my opinion is if they (Europe) get out of of their own way,” Trump Jr. said during a business discussion in the northwestern Bosnian city of Banja Luka, according to video recordings provided by the official television RTRS television.

Banja Luka is a key city in Republika Srpska, the Serb-run part of Bosnia, whose leaders are staunch admirers of U.S. President Donald Trump and Russian President Vladimir Putin.

The press office of the U.S. Embassy in Sarajevo, Bosnia’s capital, told The Associated Press in an email that Trump Jr. came “in a private capacity.” The visit was nonetheless seen here as a boost for the Serb separatist political leadership.

Trump Jr.’s trip came as U.S. Vice President JD Vance traveled to Hungary to support the reelection bid of nationalist Prime Minister Viktor Orbán before a highly-contested vote next weekend.

Bosnian Serb politician and former Republika Srpska president, Milorad Dodik, an ally of Orbán, said on X that the two visits “signal an important shift of the U.S. administration under the leadership of President Trump and the care for this part of Europe regarding the position of Christians.”

Trump Jr,, in Banja Luka, said that eastern European countries “have a work ethic that has (withstood) some of the ‘woke’ nonsense that has really been a parasitic thing in the mind in Western Europe.”

“I see that creating major fractures in the European Union between those few countries in eastern Europe that actually still believe in common sense, and Western Europe that’s clearly missing in the political discourse these days,” he said.

Dodik has repeatedly called for the Serb-run half of Bosnia to break off from the rest of the country that is run by Bosniaks, who are mainly Muslims, and Croats. The Serb bid to form its own state and unite with neighboring Serbia was seen as the main cause of the 1992-95 ethnic war that killed more than 100,000 before ending in a U.S.-brokered peace agreement.

The Biden administration in 2022 imposed sanctions on Dodik and individuals and companies linked to him because of the separatist policies that stoked fear of renewed instability. The sanctions were lifted by the Trump administration last year.

The Trump administration has long been critical of the EU, notably over trade and EU regulation of the technology sector. Its criticism of long-time European allies has intensified during the Iran war.

Bosnia is a candidate country for EU membership and the 27-nation bloc says it’s Bosnia’s biggest trading partner, investor and provider of financial aid.

What this borrowing (and its related interest payments) will ultimately mean for the economy remains to be seen: Theories range from a market “reckoning” through to public investment being crowded out by spending on debt maintenance. Others suggest inflation will merely be allowed to rise, ultimately lowering the real value of the debt.

JPMorgan Chase CEO Jamie Dimon, however, is alarmed: The Wall Street veteran knows better than to predict when the issue may come to a head—but he is certain that the nation’s fiscal trajectory cannot be ignored forever.

“The best way to deal with the problem is to actually deal with the problem, to acknowledge it, to work on it,” Dimon told NPR’s Newsmakers podcast. “Years ago, we had a solution, the Simpson-Bowles Commission. It didn’t get done. I wish it had gotten done. It would have been a home run for all of Americans, and it would have resolved some of these issues.”

Dimon was referring to the work of President Obama, who oversaw the creation of the bipartisan National Commission on Fiscal Responsibility and Reform, commonly known as the Simpson-Bowles (or Bowles-Simpson) Commission. The ensuing report made several recommendations: cutting discretionary spending, reforming tax law, and reshaping health care spending.

While many of the suggestions from the commission have proved a basis for policy arguments when it comes to government spending, none of the conclusions of the report were ever formally brought into law.

Dimon highlighted that a vast chunk of government spending (and hence, borrowing) is “set in stone” because it relates to Medicare, Medicaid, and Social Security. According to the Congressional Budget Office’s (CBO) most recent full-year calculations, this mandatory spending accounted for $4.2 trillion of a total $7 trillion spending for 2025.

“I think we should work on it, but I don’t know—and again, I don’t think anyone can predict: Does it become a real problem in six months, six years? I don’t know—I do know it will become a problem, and the way it would exhibit itself is volatile markets, rates going up … bond vigilantes, people not wanting to buy United States Treasuries, [the U.S.] will still be the best economy, but they’ll not want to own U.S. Treasuries,” Dimon explained. “So we should deal with it sooner than later maybe, and if it gets done that way, it’ll be kind of crisis management which we’ll get through—it’s just not the right way to do it.”

A bipartisan issue

Over the years, both Republicans and Democrats have failed to meaningfully address the issue.

Proposals have been put forward by independent groups: The Committee for a Responsible Federal Budget has continually advocated for a federal unified budget deficit at or below 3% of GDP. (At the moment it’s around 6%.) This idea has been backed by Rep. Bill Huizenga (R-Mich.) and Rep. Scott Peters (D-Calif.), the cochairs of the Bipartisan Fiscal Forum. Indeed, the entire steering committee for the forum has supported the notion and introduced a resolution to that effect.

“Neither Democrats or Republicans have really focused on this for a while. It comes up all the time and you talk and you walk the halls of Congress, I mean, almost everyone knows,” Dimon added. “It’s just we haven’t had the will yet to actually deal with it, and it’s unfortunate because it can end up with a real problem, worse than it would otherwise have been. Good policy is free.”

Indeed, economists and analysts aren’t necessarily worried about the level of government debt, rather the debt-to-GDP ratio. Depending on who you ask, the debt-to-GDP ratio stands at around 122% of GDP at present. This measure demonstrates an economy’s spending versus its growth, and the risk associated with lending to a nation that isn’t growing fast enough to handle its spending. To rebalance that ratio, an economy could either cut spending or increase growth—the latter being by far the less painful option.

Dimon is bullish on the strength of the U.S. economy, saying it should aspire to hit 3% growth if not “even better than that.”

“If we grew at 3% and not 2% … the debt to GDP would start going down,” he added. “This is the most innovative nation the world’s ever seen. And so I think we should focus a little bit in that to solve the problem too, not just raise taxes or cut expenditures.”

The publishers, music producers, and film directors who make up the creative economy would say yes — as would many of the artists and writers they work with. But some in Big Tech are beginning to push back, arguing that ideas—like information—should be free, accessible, and repurposeable for anyone. When it comes to ideas, they argue, even those which spring directly from our own heads are the product of every other idea, environment, and person we’ve come into contact with. As such, they are fair game for training the large language models (LLMs) behind the AI platforms many of us have become reliant upon.

The argument has become increasingly urgent as generative AI companies build powerful models—and attract huge investment—by ingesting vast amounts of online text, images, and video, including books, journalism, and art created by humans.

This is the existential issue facing, among others, the international publishing giant Hachette. David Shelley, the company’s U.K. chief who also became U.S. CEO in January 2024, is joining the fight on behalf of creatives everywhere.

Shelley is a publisher through and through. The son of antique booksellers, he grew up above a bookshop and got his first industry role fresh out of university. You would be hard-pressed to find someone more passionate about, and invested in, the future of publishing. “We’re at an absolutely pivotal moment,” he says. “We need to stand up for the rights of the authors we work with and for the whole of the creative industries.”

Hachette vs. Google

This is not mere lip service. This January, Hachette asked a U.S. federal court for permission to intervene in a proposed class action lawsuit against Google. Along with Cengage, an education technology provider, the publisher claims the tech giant copied content from Hachette books and Cengage textbooks to train its large language model, Gemini, without asking permission. Google argues that training LLMs on vast text-based datasets is a transformative process which analyzes patterns in language, rather than reproducing the original works and, as such, qualifies as fair use.

Shelley isn’t buying it. “It’s just another form of theft,” he says. “We know these LLMs basically stole our authors’ work.”

This isn’t the first time Hachette has taken legal action against those looking to steal from it. In 2023, the company took on Internet Archive, an online library which offers users a free, digitized archive of music, books, and other publications. Hachette, along with Penguin Random House, HarperCollins, and Wiley, claimed the platform allowed people to download copyrighted books for free, against the authors’ wishes. In March 2026, Hachette Book Group, the American arm of the business, took on what it alleges is a pirate site, Anna’s Archive, for the same reasons.

Hachette has an impressive portfolio to protect. As one of the Big Five major global publishing houses, it is the force behind bestsellers from Donna Tartt’s The Goldfinch to Stephenie Meyer’s Twilight saga, as well as nonfiction titles such as Malcolm Gladwell’s Outliers and Mitch Albom’s Tuesdays With Morrie. Parent company Hachette Livre’s 2025 revenues exceeded €3 billion ($3.44 billion), driven by the work of popular authors across the 13 regions it operates in.

The Google lawsuit is just one of many examples of creatives taking on Big Tech. Across the U.S. and Europe, dozens of lawsuits have now been filed by individuals and organizations seeking to stop AI companies from training their models on copyrighted material without permission.

62%

Revenue growth since Shelley took the helm

€3 billion

Total revenue for Hachette Livre in 2025

14%

Hachette’s share of the U.K. publishing market

Last year, three authors won a landmark victory against AI company Anthropic, resulting in a $1.5 billion settlement. It is worth noting, however, that they did not win on the grounds of breach of copyright. The judge ruled that Anthropic’s use of the authors’ work was “exceedingly transformative” and therefore allowed under U.S. law. Unfortunately for Anthropic, over 7 million of the books it had used to build its training library were pirated copies, each of which carried a potentially steep penalty.

For Shelley, this is really an issue of semantics. “Copyright and piracy often go hand in hand,” he says. He cites children’s writer Enid Blyton’s estate, which the publisher owns, as an example. “Blyton spent her whole life writing those books — that was her achievement. If you can then ingest those into an LLM and the model can use that to create copies, to me, it’s very clear that it’s her intellectual property that has been ingested and is being monetized.”

And here is the crux of the issue. Someone is making money from the use of these ideas—but it’s not the author, it’s the LLM companies. The commercial stakes are enormous: the global generative AI market was valued at $103.58 billion in 2025 and is projected to be $161 billion in 2026, according to Fortune Business Insights.

“Success in this lawsuit would be recognition that our creators’ work belongs to them, and they must be able to decide what is done with it,” says Shelley. “So, if they want to allow a platform to use it for the LLM, they should be remunerated for that. Or they should have the right to say, ‘I do not want my work to be used in that way.’”

And lawsuits such as this one are about far more than a single company or an individual artist. At stake is the economic model that underpins the entire creative industry.

The future of the creative economy

Shelley does not mince words when describing the current approach many AI companies are taking when it comes to intellectual property. “It’s basically parasitic,” he says. “The monetization happens from the tech platforms—the fans are still getting content, but that content is based on original creative work by humans who get nothing for it.”

And if it should be allowed to continue? “It would be completely devastating,” he says.

The current creative ecosystem is simple but effective. Creators use their imaginations to create things; organizations such as publishers partner with them to distribute those things. People pay to consume the creations, and both publisher and creator get a share of those sales. “[But] if the writers aren’t getting any money, frankly, then we aren’t getting any money—and then what is the point of publishing houses if there’s no income stream?” he says.

While few would feel compelled to pull out their tiny violins for the fate of multibillion-dollar businesses in this situation, the consequences could be far more serious, Shelley points out.

One logical conclusion is a return to the early days of publishing, when only the super-wealthy (or those lucky enough to have a rich patron) could afford to write for a living. Whether it is writing or music or illustration, “the fact you can make a good living in all of these fields is a really strong incentive,” says Shelley. Without the economic model, “the talent pool shrinks.”

Worse still, we face a future where the only art available is an iteration of an iteration on an iteration. “LLMs are just predictive text,” says Shelley. “If you starve the supply, then there will be no new stories. As humans, we need new stories, we need new art, we need new ideas, and to get that, the economics need to work for the people who make those things.”

What is most frustrating for Shelley is that there already exists a robust mechanism for ensuring this doesn’t happen: copyright law. “Copyright essentially exists to ensure creators are able to earn a living,” he says. “I don’t think it needs to change, but it does need to evolve.”

Our legal system often operates by looking at precedent, and it is here that Shelley sees some hope. He cites high-profile music cases, such as Pharrell Williams v. Bridgeport Music, in which the producer-songwriter and artist Robin Thicke had to pay millions of dollars in damages to the estate of Marvin Gaye for mimicking the “feel” of some of Gaye’s work in their 2013 hit “Blurred Lines.”

“It’s not an exact science,” says Shelley. “But there is enough case law now to say, ‘This is what’s right.’ Not everyone will agree with every judgment, but there is a framework in place.”

How Hachette is using AI

Shelley is also realistic about the need to work with Big Tech in order to achieve Hachette’s mission (“to make it easy for everyone to discover new worlds of ideas, learning, entertainment, and opportunity”).

“As business leaders, we need to be able to hold lots of contradictory ideas in our head at once, and we need to have nuanced relationships,” he says. For publishers, that tension is particularly acute: The technology platforms Hachette is challenging in court are also vital in shaping how readers discover books—from search engines to social media communities like TikTok’s BookTok.

Pharrell Williams was one target of a copyright lawsuit and had to pay millions in damages for imitating the “feel” of a Marvin Gaye song.

David Buchan—Getty Images

He points out that no company in the digital age can afford not to work with the likes of Google, even if it disagrees with certain elements of the platforms’ operation. In an ideal world, the key is to work with the platforms to make systems more fair for everyone.

Neither can companies afford to shy away from the transformative potential of AI, however cynical they may be about the motives of the platform owners. For Shelley, the key is to have very clear boundaries from the start, about where the publisher will and will not use the technology.

“We will use it operationally, where we think it helps to get a writer’s work to more readers,” he says. At Hachette, that means implementing it for heavy-lift data entry, such as bibliographic metadata required for online shops; warehouse-demand planning; and simple customer service matters such as “When will my books arrive?” queries.

Where the company will not embrace AI’s usage is in creation. “We have literally no business without authors, translators, illustrators, and the wider creative economy,” says Shelley. “We are very clear about AI not competing with them.” I ask whether this means that Hachette would make the decision never to publish AI-written books, and his answer is clear: “Yes. I don’t see the value in that at all.”

Indeed, there is a growing trend on both sides of the Atlantic for using human creation as a badge of honor. In early 2025, the U.S.-based Authors Guild launched a “Human Authored” certification, with the U.K.’s Society of Authors following suit in March 2026. The certification allows for minor AI assistance—such as spell-checking or brainstorming—but the text itself must be human-written.

As with the hipster revival of the word “artisanal” in the mid-2000s, the AI age is beckoning in new terms to connote great value and desirability. Now, instead of coffee made from rare Southeast Asian beans or blankets knitted in little-known Nordic communities, the focus is on content. From books to marketing campaigns, experts suggest that, in a world flooded by AI-generated work, those who can will pay for what is being called the “human premium” by some thought leaders.

Protecting creativity, a call to arms

Of course, business leaders must play their part in protecting the economic ecosystem that makes this possible.

To these leaders, across industries, Shelley is using the Google lawsuit to issue a rallying cry: “Look, it would be totally disingenuous of me to pretend I wasn’t trying to preserve our business, but fundamentally I think it will be an enormous loss to society if copyright law were to be ignored.”

He explains that publishing can be something of a “quiet industry,” but for an issue of this magnitude, it’s crucial to get past the discomfort of speaking out. He is calling on leaders to lobby governments; do crucial public affairs work; talk to the press about issues that matter; and where necessary, pursue legal action.

“The nature of a changing world—particularly when it comes to one governed by technology—is that you have to keep litigating,” he says. “It’s a crucial way of updating case law. People take copyright for granted, but it came about through humans lobbying for it.”

This is, in some ways, easier to do in the States, where the culture of litigiousness means the process is more common. There are, however, some societal trends which make the battle seem more daunting. “One of the issues we’re experiencing in the U.S. is book banning,” says Shelley.

Here, again, is an issue which appears, on the surface, to be unique to the publishing industry, but which could have severe consequences for businesses of all sectors. For Shelley, freedom of expression is no longer merely a cultural issue—it is a leadership and governance one.

“A workplace is not a hermetically sealed environment,” he says. “All business is reflective of everything that’s going on in the wider world.” The real risk for leaders is a future workforce of people who cannot or will not challenge their own preconceptions; who cannot embrace new ideas or work well with those whose views differ from their own. The downside of the hyper-personalization of content that LLMs allow is the creation of echo chambers, where consumers are fed ideas which already mirror their own. In banning books or limiting the possibility of new stories from a diverse range of sources, society risks losing generations of free thinkers.

“There are some things where you feel you’re just doing your job and it’s just business, and some where you feel a sense of mission,” says Shelley. “For me this is both. I feel so strongly from a business point of view and a moral and societal point of view that there will be bad outcomes if we don’t step up.”

200 years of great ideas

When Louis Hachette opened his titular bookshop in Paris in 1826, it is unlikely he could have foreseen how global his legacy would become. The publisher, which now exists as Hachette Livre in Europe and Hachette Book Group in the U.S., is owned by French multinational Lagardère, which is, in turn, owned by Fortune 500 Europe member, the Louis Hachette Group.

The business operates in 13 regions, from its native France to New Zealand, China, and sub-Saharan Africa. Its sub-brands include heritage publishers such as Hodder & Stoughton and John Murray (which published the first edition of Charles Darwin’s On the Origin of Species), and its titles, from Hamnet to The Queen’s Gambit, have been transformed into some of the most talked-about film and TV in recent years.

The bookshop that started it all. Brédif, which later became L. Hachette et Compagnie, was founded by Louis Hachette in 1826 in Paris’s Latin Quarter.

Courtesy of Hachette

Given Hachette’s French roots and global outlook, some might find it surprising that Shelley’s English-language section of the business is a major growth driver.

But Shelley has form when it comes to making publishers money. At age 23, he took the helm at Allison & Busby in 2000 and needed just five years to take the publisher from heavy losses to profitability. Now he is having a similar impact at Hachette. By the end of his first year as head of Hachette Book Group, sales were up 7% on 2023. And 2025 was another bumper year for Lagardère, with revenues growing by 3%, driven largely by the success of Shelley’s operation.

When I ask Shelley how he balances innovation with a 200-year-old legacy, his answer comes not in the lofty language of ideas and freedom of expression but in terms much more common to today’s business world. “I believe very strongly in being customer-obsessed,” he says. “It’s about giving consumers what they want, being where they are, and not being too protectionist or tastemaking about it.”

In practice, this does mean embracing all things digital. Shelley describes Hachette as being “forensic” about removing friction for readers, doubling down on ebooks and audiobooks across a range of platforms. But it also means the opposite: betting big on analog. Across the U.K. and the U.S. markets, Hachette is exploring a range of adjunct products, including jigsaw puzzles, tarot cards, and luxury stationery, as consumers increasingly seek out ways to log off from the online world. It is also investing in making books that are beautiful objects in and of themselves, such as special editions with sprayed edges and their own display boxes.

And true to Shelley’s ideal of serving customers rather than trying to shape their tastes, Hachette is also expanding its range of “romantasy” titles—the romance-fantasy genre which is a firm favorite of the BookTok community.

Whether such moves are enough to safeguard the company at a time when its lifeblood is increasingly under threat remains to be seen, but Shelley is optimistic.

When it comes to copyright law, “we have something that is so fit-for-purpose, that has served humanity so well for such a long time, all we need is a slight evolution,” he says.

“If our eventual aim is for creators to be able to benefit from their ideas then that’s the place we’ll end up.”

Last week, in Queens, I met up with Infinite Machine CEO Joseph Cohen at his startup’s new vibey office space in Long Island City. After a brief tour, Cohen and I donned motorcycle helmets and went for a ride, spinning through the cobble and paved roads and bike lanes on Infinite Machines’ new e-bike, the Olto. The Olto is quick, fun, and smooth, and it was a blast.

As Cohen and I waited at a traffic light, people on the corner pointed at us, grinning. Olto’s sleek and modern design—like a Cybertruck for the bike lane—tends to grab attention. But is it really a bike?

The Olto follows all the technical parameters of a Class 2 e-bike, where you don’t need a license plate or registration, and it’s allowed in the bike lane. Legally, it’s a bike. In motion, it felt more like I was riding a moped. The Olto is a whopping 176 pounds, has a moped-style seat position, and uses a throttle that gets it up to 20 miles per hour—or more if you’re in a city like New York where higher speeds are allowed.

While there technically are pedals, Cohen advised me not to use them, and said that customers keep the pedals in the locked position—like pegs. Almost as proof of this, the chain on the Olto I rode was really rusty, and a piece of black plastic covered most of it, which I couldn’t help but notice would make the chain impossible to lube or service.

Courtesy of Infinite Machine

For Cohen, these quirks are exactly the point. He and his brother, Eddie, wanted to design a brand new kind of two-wheel transit option designed for both the road and the bike lane. The two spent a lot of time riding their Vespas during Covid, and Cohen says they realized “that two wheels is kind of a hack for New York.” Infinite Machine started manufacturing its first vehicle, an electric moped the P1, and later this e-bike Olto, which they started delivering to customers last year, though he wouldn’t tell me how many had been sold yet

Infinite Machine, which launched a moped motorcycle before the Olto, is already dabbling in what other kinds of vehicles it can build next—and how the startup could (eventually) plug in some sort of autonomy to its e-bikes and scooters. It’s a well-funded venture, with $14.2 million from investors including a16z’s American Dynamism fund (a little funny when you consider that Infinite Machine, like many transit companies, has its scooters and e-bikes assembled in Shenzhen, China). Cohen and his brother, Eddie are energetic and bubbly about their sleek designs and where they see the future of transit going. When you’re talking with them, it’s hard not to get excited right along with them.

At the same time, it’s hard to imagine Infinite Machine won’t run into some trouble as they scale. The e-mobility space is notoriously difficult and full of cautionary tales, but more than that, I wonder what the reaction will be from cyclists like me to have something like Olto passing them in the bike lane. At a speed of 20 or 25 miles per hour, a 176-pound bike carries much more energy than a traditional bicycle, and collisions don’t look the same. E-bike accidents are drawing additional scrutiny from residents in cities, including New York, where some groups are pushing for more parameters for e-bikes and scooters.

After thinking all of that over for a few days, I called up Cohen yesterday and asked about some of those concerns. He said that Infinite Machine is proactive with regulators and has built a “good relationship” with the New York City transportation department, and pointed out that he hadn’t heard of any complaints so far. From his perspective, he wants customers to ride in the bike lanes as a safety precaution from cars and dangerous drivers. “The real threat to safety is from cars and trucks, not from e-bikes,” he said.

Olto isn’t the only vehicle that may redefine the bike lane. Last week, I saw Amazon’s new four-wheel “e-cargo quadricycle” pedaling through the Lower East Side and making last-mile deliveries. It’s a stretch, but the enormous quadricycle technically meets all of the qualifications of a bike, even though it weighs many hundreds of pounds.

It’s hard not to feel that these new modes of transportation may erode the social order of the bike lane—the idea that bike lanes are solely for lower-speed vehicles and the commuters who are most vulnerable on the road. I’m a cyclist with four bikes—I use bike lanes all the time—and can’t help but wonder as some of these new designs get prolific, whether it could start to feel hostile to the people who are actually pedaling.

Joey Abrams curated the deals section of today’s newsletter.Subscribe here.

VENTURE CAPITAL

– E2, a Menlo Park, Calif.-based developer of medical technology designed for venous thromboembolism, raised $80 million in Series C funding. GildeHealthcare and Norwest led the round and were joined by existing investors.

– TrueFootage, an Austin, Texas-based residential appraisal and appraiser services company, raised $40 million in Series C funding from CoxEnterprises, NavaVentures, RogerFerguson, PilotEnterprises, and others.

– MembraneTechnology & Research, a Newark, Calif.-based industrial membranes company, raised $27 million in Series B funding. ClimateInvestment led the round and was joined by HartreePartners.

– HexemBio, a New York City-based biotech company focused on blood stem cell rejuvenation therapy, raised $10.4 million in seed funding. DraperAssociates led the round and was joined by SOSV, Seraphim, and others.

– CONXAI, a Munich, Germany-based agentic AI platform designed to automate construction workflows, raised €5 million in pre-Series A funding. BayBGVentureCapital and CapricornPartners led the round and were joined by PiLabs, Earlybird, Noa, ZacuaVentures, and ArgonauticVentures.

– FLORAFertility, a Calgary, Canada-based fertility insurance platform, raised $5 million in seed funding. ManchesterStory led the round and was joined by Slauson & Co., BDC, MarathonFund, and AdaraVenturePartners.

– Felix, a Prague, Czech Republic-based AI workflow platform designed for legal, finance, and insurance professionals, raised $1.7 million in pre-seed funding. XYZVentureCapital led the round and was joined by angel investors.

– PrismLayer, a Washington, D.C.-based AI-powered platform for enterprise risk management, raised $1 million in pre-seed funding. FenwaySummer led the round and was joined by PluralVC and others.

PRIVATE EQUITY

– BayCollective, backed by SixthStreet, agreed to acquire Sunderland AFC Women, a Sunderland, U.K.-based women’s soccer club. Financial terms were not disclosed.

– Caylent, backed by GryphonInvestors, acquired Pronetx, a Columbia, Md.-based customer experience consulting firm. Financial terms were not disclosed.

– FirstReserve acquired a majority stake in LindseySystems, an Azusa, Calif.-based designer and manufacturer of electric transmission and distribution equipment. Financial terms were not disclosed.

EXITS

– GamutCapitalManagement agreed to acquire AcoustiEngineeringCompany, an Orlando, Fla.-based ceiling, drywall, flooring, and specialty interior services provider, from Ardian. Financial terms were not disclosed.

– TritonPartners agreed to acquire Integris, an Amsterdam, The Netherlands-based ballistic protection company, from AgilitasPrivateEquity. Financial terms were not disclosed.

FUND OF FUNDS

– Eclipse, a Palo Alto, Calif. and New York City-based venture capital firm, raised $1.3 billion across two funds focused on companies in physical industries.

PEOPLE

– 500Global, a Palo Alto, Calif.-based venture capital firm, hired NadiaKarkar as managing partner. Previously, she was with TPGRise.

– H.I.G. Capital, a Miami, Fla.-based private equity firm, promoted BrianSchwartz to CEO.

– RallyVentures, a Menlo Park, Calif.-based venture capital firm, hired LizBenz as operating partner. Previously, she was Chief Sales Officer at Jamf.

When Bed Bath & Beyond announced last week it was buying the Container Store for a pittance, CEO Marcus Lemonis touted the deal as a key component of his plan to create a home-oriented conglomerate that includes retail brands, home services, installable products such as flooring and cabinetry, insurance, and more.

“We are building the first Everything Home Company,” he said in a release, explaining that it is “designed to make home ownership and living simpler and more affordable through a disciplined, interconnected ecosystem.”

Snagging the Container Store for $150 million, a fraction of its market capitalization high of $1.64 billion more than a decade ago, will allow Bed Bath & Beyond to add the popular modular storage system Elfa and the higher-end customizable Closet Works service to its array of offerings. And—excitingly for those nostalgic for Bed Bath & Beyond’s candle-scented stores, the last of which closed in 2023 following the chain’s bankruptcy filing—the move will be a return to brick-and-mortar retail: The 100 Container Store locations will be rebranded as The Container Store / Bed Bath & Beyond.

Overstock.com purchased the company after its spectacular flame-out three years ago, then changed its name to Beyond Inc, and then last year to Bed Bath & Beyond. Other brands under the BB&B umbrella include BuyBuy Baby and Brand House Collective, a home furnishings company previously called Kirkland’s Home.

Lemonis deserves credit for having a vision for what the company’s components could amount to in the aggregate. But there was some skepticism from Wall Street about the move. Morningstar analyst David Swartz told real estate industry publication CoStar News that Bed Bath & Beyond was “a conglomerate of failing businesses,” and that he wasn’t surprised that investors were balking at Lemonis’ strategy. (Shares are down 15% since January, when Lemonis became CEO after first serving as executive chairman.) GlobalData managing director Neil Saunders has called the company “a bit of a hodgepodge” collection of brands.

And indeed, both Bed Bath & Beyond and the Container Store, which had its own bankruptcy in late 2024, are weak businesses that are a fraction of the size they were at their peaks. When brands are struggling, one plus one is unlikely to equal three.

What’s more, it does not appear to have been smooth sailing behind the scenes at Bed Bath & Beyond. The company has undergone a few rebrands, churn in its C-suite, and quick changes in strategy—offering little evidence of the internal cohesion necessary to make a portfolio of brands gel.

There is no shortage of cautionary tales of retail industry marriages that went awry: Men’s Wearhouse’s acquisition of Joseph Abboud in 2013 yoked together two brands struggling for growth, and it was not transformative for either. Canada’s Hudson’s Bay Company conglomerate, long gone, brought a number of department store chains, all having a hard time—The Bay, Lord & Taylor and Saks Fifth Avenue—in different countries under one portfolio company; most have sought bankruptcy or gone out of business. Even a broadly well-run company like Tapestry can struggle to integrate a weak business: It has taken a few write-downs on its 2017 acquisition of Kate Spade.

However good Lemonis’s vision might look on paper, he’ll have to act fast to show it works: Bed Bath & Beyond had net income losses totaling $650 million, on revenue of $4 billion, in its last three full years.

Kevin Koenig, a Connecticut-based yacht consultant, was recently helping a prospective client buy his first boat. Koenig nurtures a 278,000-strong Instagram community under the handle @theyachtfella. The Yacht Fella is also a Watch Fella, and he and his client got to talking, as horology nerds do, about their metal. “I asked him what his ‘daily’ is,” Koenig recalls.

To his yacht-aspiring wrist, the buyer buckles a Rolex Oyster Perpetual Explorer II, a watch designed to commemorate Sir Edmund Hillary’s 1953 summit of Everest. Turns out Koenig’s daily is also a Rolex Explorer II, though his model is the Polar, whose avalanche-white face is coveted by collectors. Regardless: Twinsies! Said Koenig to his fellow explorer, “I knew I liked you.”

Neither Koenig nor his buyer has plans to trek to Everest or, per Rolex, “into the unknown, where the boundary between night and day is blurred.” But the Explorer II binds the men in a common narrative—that if they wanted to, their timepiece would have a glow-in-the-dark Chromalight display to aid their perilous ascent.

That feature is what’s known in horology as a “complication.” The term encompasses everything from second hands to details that follow the positions of planets; it can be as straightforward as a GMT (Greenwich Mean Time) hand that tracks an alternate time zone or as intricate as a tourbillon, a byzantine mechanism that counteracts the effect of gravity on timekeeping.

Unlike in most relationships, complications in the timepiece world are highly desired. They hint that the wearer has stories to tell, that they’re the type who needs to know the exact time in Berlin while they’re lingering over omakase in Vancouver. They also signal a connoisseur’s appreciation for the kind of exacting craftsmanship that only a human can execute.

Rolex’s Explorer II, and Jaeger-LeCoultre’s 2025 Reverso Tribute Geographic.

COURTESY OF ROLEX ; COURTESY OF JAEGER

Collectors covet these pieces, explains Yoni Ben-Yehuda, head of watches for luxury retailer Material Good, because “similar to the handmade stitches on a Birkin bag, machines simply cannot do these complications”—a comforting notion and powerful value proposition as we cruise, driverless, toward an AI-slopped horizon.

Material Good runs four Audemars Piguet joint-venture boutiques in the U.S. and a forthcoming Vacheron Constantin shop in Aspen. These venerable Swiss houses represent peak legacy watchmaking, and their most expensive and rarest pieces tend to be deliciously complicated. (Vacheron Constantin’s Solaria Ultra Grande Complication La Première, rolled out last year, incorporates a mind-bending 41 features.) Compared with their tourbillons and minute repeaters, a seconds-counting hand is peasant fare. “A complication, the way it is used in our nomenclature, is a watch that is complex,” Ben-Yehuda says.

A complication needn’t be that intricate to add value. Colored a prominent tangerine, the additional hour hand on the Explorer II pops against the black or white face and points to a 24-hour bezel. It provides a clearer way to keep time in extreme environments, but Koenig, who’s on the road 120 days a year, finds utility for it as a reminder of his home base. By rotating the bezel to local time in London, say, or Dubai, he can make sure the orange hand follows the local zone, while the primary hand remains on Greenwich (Connecticut) time.

“No one needs these timepieces. Our phones will keep more accurate time. This is about beauty, emotional connection, the transmission of community.”

Yoni Ben-Yehuda, head of watches, Material Good

But that’s also kind of a 101 complication. According to Ben-Yehuda, the industry threshold for intricacy is the perpetual calendar, a constellation of sub-dials tracking day, month, year (even leap years) and sometimes moon phase. “If civilization shut down the way we know it, those perpetual calendars, which keep accurate time for 104 years without any use of computing, would become one of the most important instruments on earth. They connect us to the cosmos,” he philosophizes, “to something bigger than us.”

Watches are time-telling instruments, but more important, storytelling instruments. “No one needs these timepieces,” says Ben-Yehuda. “Our phones will keep more accurate time. This is much more about beauty, emotional connection, the transmission of community.” And the nichier the complication—from the regatta timer (a bidirectional rotating bezel) of the Rolex Yacht-Master for sailboat racers to the planetary orbit positioner on the star-sprayed dial of Van Cleef & Arpels’s seductive Midnight Planétarium—and the greater number of them on a given piece, the more Shakespearean the tale the watch tells.

Vacheron Constantin’s Solaria Ultra Grande Complication La Première, Daniel Roth’s Rose Gold Tourbillon.

COURTESY OF VACHERON CONSTANTIN; COURTESY OF MATERIAL GOOD

Jaeger-LeCoultre’s 2025 Reverso Tribute Geographic might announce itself as a svelte Art Deco companion whose reversible face reveals a world clock for a gentleman-athlete to keep time across the British Empire. Vanguart’s spellbinding Black Hole Tourbillon, with its time-winding joystick and virtuosic levitating tourbillon, might entreat collectors: Peer into my vortex of descending graduated discs, a mysterious galaxy of 755 pieces, where only the true masters of the universe govern time and space.

It’s these complex watches that get collectors in the $60 billion luxury watch market hot and bothered. At Sotheby’s, the December Fine Watches auction brought in $42.8 million, and included a Patek Philippe with a cloisonné world-time complication and fittingly envy-green alligator strap. “Niche areas of [watch-collecting] have grown in popularity,” timepiece journalist Caleb Anderson wrote for Sotheby’s, “with collectors and enthusiasts being drawn to objects that serve as artistic and horological showcases both of themselves and of their wearers.”

Put more plainly by Ben-Yehuda, “Super-collectors look for those design cues to delineate between good and great watchmaking. That is one of the reasons one watch costs $15,000 and a watch with the same quote-unquote complication costs $50,000.”

“And people that know watches know what you spent on that complication,” Koenig says, summarizing this society’s joystick-measuring tendencies. “Watch culture is, for better or worse, a flex culture.” Horological equals, he and his yacht-seeking Explorer II buddy closed the deal.

Luxury timepieces

Five watches worth a complicated relationship

1. Rolex Explorer II From $10,600 Are you afraid of the dark? Not with this Rollie, whose abyss-black or snow-white dial hosts three hands and hour markers that, like a bioluminescent deep-sea creature, emit a blue glow in the absence of light.

2. Jaeger-LeCoultre 2025 Reverso Tribute Geographic From $22,800 Never be late for a regatta in Rio or cocktails in Karachi, two global destinations on the 24-hour world clock and map hiding on the rear face of Jaeger-LeCoultre’s slim Reverso Geographic, available in stainless steel or 18-karat pink gold.

3. Audemars Piguet Royal Oak Perpetual Calendar Champagne Dial $125,000 The yellow gold and chunky silhouette would look good on Tony Soprano, but the perpetual calendar—including a dreamy moon-phase complication—in the octagonal Champagne dial of AP’s 1972 design gives it a more-than-meets-the-eye intellectual quality.

4. Daniel Roth Rose Gold Tourbillon $212,000 A pioneer in the independent watchmaking world in the 1980s and ’90s, this Swiss maison (and its signature double-ellipse dial) now lives on as part of Louis Vuitton’s Fabrique du Temps, which just debuted a pair of individually numbered knockouts. The tourbillon version encases an appealing tension between the 270-piece complication’s visceral architecture and Roth’s flair for aristocratic typefaces and theatrical curves.

5. Vanguart Black Hole Tourbillon From $455,000 With concentric hour, minute, and tenths-of-a-minute discs surrounding a hypnotic levitating tourbillon, the futuristic Black Hole evokes the contraption that frees the baddies at the climax of the movie Thirteen Ghosts. Available in titanium or rose gold and with Arabic numerals.

This article appears in the April/May 2026 issue of Fortune with the headline “Taking time to tell stories: Why ‘complex’ is the new flex for watch fans.”

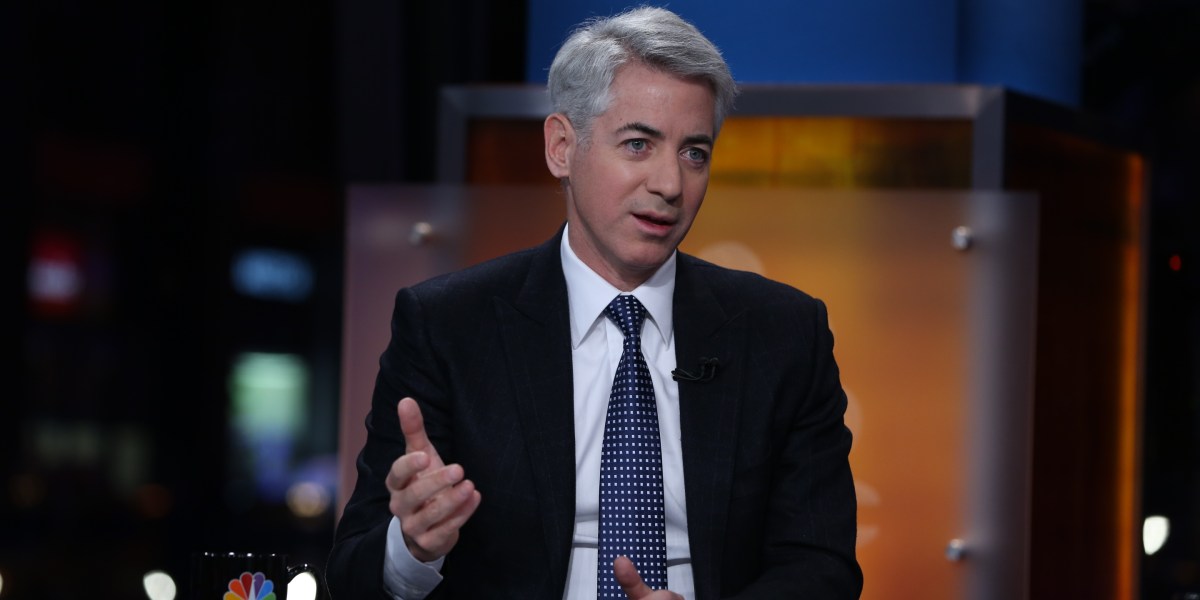

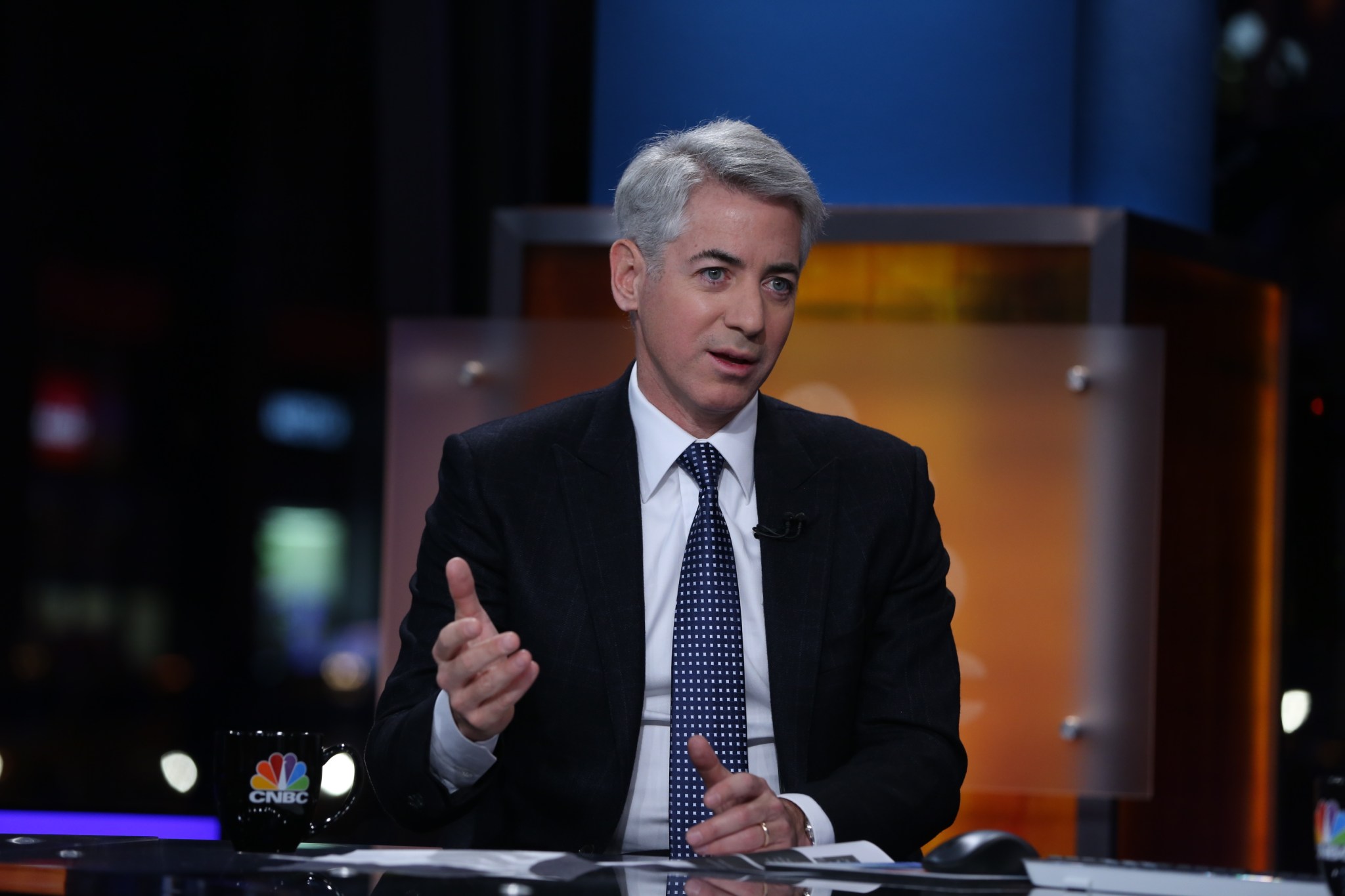

Billionaire investor Bill Ackman’s hedge fund, Pershing Square Capital, is planning to buy Universal Music Group (UMG), the world’s largest music company, which represents artists including Taylor Swift, Bad Bunny, Bob Dylan, and the Beatles.

The $64 billion pitch announced Tuesday is Ackman’s latest move to turn Pershing into a “modern-day” Berkshire Hathaway and make him the next Warren Buffett. Pershing currently controls 4.6% of UMG shares. The deal would merge UMG and Ackman’s Pershing Square SPARC Holdings as a joint entity to be listed on the New York Stock Exchange by the end of the year.

“The company’s management have done an excellent job nurturing and continuing to build a world-class artist roster and generating strong business performance,” Ackman said in a statement. “However, UMG’s stock price has languished due to a combination of issues that are unrelated to the performance of its music business, and importantly, all of them can be addressed with this transaction.”

The move comes weeks after Pershing filed to be listed on the New York Stock Exchange, marking Ackman’s latest attempt to go public in the U.S. The hedge fund has a market cap of $11.27 billion, $28 billion in assets under management, and Ackman is worth $8.13 billion.

Ackman, a self-described “Buffett devotee,” is following in his idol’s footsteps by attempting to acquire UMG. The IPO and joint listing with UMG would help Pershing gain access to “permanent capital,” a key part of Buffett’s investing playbook. Investors can pull their money out of a hedge fund quarterly or annually, requiring fund managers to keep cash on hand and putting them at risk of having to sell their holdings. After the IPO, Pershing would have access to capital in its closed-end fund that can’t be directly revoked; investors have to sell their shares on the open market instead.

Pershing declined to comment further on the proposal. Universal Music Group did not immediately respond to Fortune’srequest for comment.

‘Be greedy when others are fearful’

Buffett, who has freely shared his investing advice for decades, is best known for one recommendation: “Be greedy when others are fearful and fearful when others are greedy.”

With this deal, it appears Ackman could be following that advice. Before the announcement, UMG’s stock, which is traded on the Euronext Amsterdam exchange, was down about 22% year to date. Today the stock is trading at 19.06 euros ($22.06), up about 2 euros ($2.32).

Pershing laid out what it sees as UMG’s weaknesses in the pitch’s announcement, explaining that the postponement of listing the company on a U.S. exchange, underutilization of the company’s balance sheet, and poor investor relations and communications are reasons for the company’s “underperformance.”

Buffett’s 1988 purchase of Coca-Cola stock stands as an instructive lesson for what Ackman is attempting with Universal Music Group. Buffett moved aggressively into Coca-Cola in the aftermath of the 1987 Black Monday crash, building a $1.3 billion stake in a brand that many investors had soured on. Just as Buffett saw Coca-Cola’s unmatched brand moat and pricing power as advantages that the market was temporarily mispricing, Ackman is betting that UMG’s enduring position in the music industry represents an irreplaceable investment that will reward patient capital.

This is not the first time Ackman has followed Buffett’s advice to take advantage of cheaper stocks, and Ackman has called on others to do the same. Last month, in a post on X, Ackman told investors to get over the war in Iran and buy Fannie Mae and Freddie Mac stocks, the two government-sponsored enterprises designed to prop up the mortgage market.

“Some of the highest quality businesses in the world are trading at extremely cheap prices,” Ackman wrote in the post. “Ignore the MSM [mainstream media]. One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend.”

When markets opened the next day, Fannie Mae’s stock market climbed as much as 41%, and Freddie Mac surged as much as 34%, the largest single-day moves for each stock since May 2025. Fortune previously reported that Ackman’s tweet was the only obvious driver of the surge.

Learning from the past

Ackman’s play for UMG requires the faith of the company’s investors, something he has fallen short of in the past. He was unable to convince Pershing’s own investors to back the company’s $25 billion IPO goal in 2024 after a series of errors. Ackman downplayed the IPO risks to investors and argued that the company could achieve a “sustained premium” to its net asset value, defying the fund’s regulatory prospectus.

The move was so disastrous that Pershing had to “disclaim” Ackman’s comments and in the following week, Ackman cut the fundraising target from $25 billion to $4 billion to $2 billion, before putting the IPO off completely.

With the hedge fund’s latest attempt, Ackman has tempered his expectations and is aiming to raise between $5 billion and $10 billion. He has changed his approach by trying to list both the closed-end fund and Pershing’s parent company. To encourage investors, every 100 shares of the closed fund they buy will automatically grant them 20 free shares of Pershing Square Capital Management.

This approach is a departure from Ackman’s past head-over-heel dealings. In 2016, Ackman stood by former investor darling Valeant Pharmaceuticals, even as criticism mounted over the company’s aggressive drug price hikes and misleading SEC disclosures. Ackman eventually reversed course and sold the stocks, but not before losing Pershing $3.2 billion.

Ackman is also known for his unrelenting attitude toward his rivals. In 2012, he began a short-selling campaign against Herbalife, which sells weight-loss shakes and vitamins. Ackman accused the company of operating illegally and of being a “pyramid scheme,” and tried to drive the company’s stock price down for five years. In the end, Ackman cut his losses, and Pershing dumped all the stock.

In 2024, six years after the dispute, Ackman relished Herbalife’s stock plunging to a 14-year low.

“It is a very good day for my psychological short on Herbalife,” Ackman wrote in a post on X six years after the dispute. “And it is an even better day for the world to see one of the biggest pyramid schemes fail.”

Correction, April 7, 2026: A previous version of this article misstated the share of UMG shares Pershing Square controls.